By

By

All Cayman entities which fall within the definition of “private fund” in the Private Funds Law, 2020 and which are carrying on business on or after February 7, 2020 have until August 7, 2020 (the “transitional period”) to register with the Cayman Islands Monetary Authority (CIMA).

The characteristics of a “private fund” are the pooling of investor funds with the aim of spreading of investment risk, where the investors do not have day-to-day control over investment decisions but instead the investments are managed by or on behalf of the operator of the fund (eg, directors or general partner) and where the “investment interests” subscribed for by investors carry an entitlement to participate in the profits and gains arising from the investments but, crucially, are not redeemable or repurchasable at the option of investors.

The Private Funds Law, 2020 therefore encompasses all Cayman Islands closed-ended fund structures, unless excluded as a “non-fund arrangement”.1

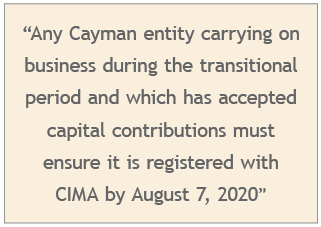

A Cayman entity structured as a private fund shall submit an application for registration to CIMA within 21 days after accepting capital commitments and must be registered as a private fund prior to receiving capital contributions from investors. Accordingly, any Cayman entity carrying on business during the transitional period and which has accepted capital contributions must ensure it is registered with CIMA by August 7, 2020.

Registration will be made electronically on CIMA’s Regulatory Enhanced Electronic Forms Submission (REEFS) platform and will require a private fund to file:

- an application form and application fee (US$366)2;

- a certificate of incorporation or registration;

- constitutional documents, such as the memorandum and articles of association or partnership agreement;

- an offering document, summary of terms or marketing materials which describe the terms of the offering;

- an auditor’s and, where applicable, an administrator’s letter of consent; and

- a structure chart showing the ownership of the private fund (excluding the investors), any subsidiaries and affiliates.

CIMA has advised that it will require a minimum of two directors for private funds structured as companies and a minimum of two natural persons in respect of a general partner of a limited partnership or corporate director. Directors appointed to “private funds” are not required to be registered under the Director Registration and Licensing Law of the Cayman Islands.

A “private fund” must have its accounts audited annually by a Cayman Islands based auditor approved by CIMA. The accounts, together with a Fund Annual Return, must be filed with CIMA within six months of the relevant financial year end and must be prepared in accordance with IFRS or GAAP of the US, Japan, Switzerland or a non-high risk jurisdiction. CIMA has confirmed that a “private fund” is required to submit an audit for its 2020 financial year. It is anticipated that CIMA will issue policies and procedures regarding waivers and extensions applicable to audits in due course.

Private funds are subject to valuation, safe-keeping and cash management requirements which will likely see appropriately qualified independent third parties undertaking such functions; although there is scope for them to be carried out in-house, by a private fund’s manager or operator or a control entity of such manager or operator, subject to certain criteria.

The valuation of the assets a “private fund” must be conducted in accordance with its valuation policy at a frequency that is appropriate to the assets held by the private fund and at least on an annual basis.

A private fund is required to appoint a custodian to hold in a separate custody account(s) in the private fund’s name, or for its account, those assets which are capable registration or of being physically delivered. The custodian must also verify that the private fund holds title to any other assets and maintain a record of such other assets.

A private fund may notify CIMA that it is neither practical nor proportionate to appoint a custodian having regard to the nature of the private fund and the type of assets held. In such circumstances, either an administrator, other independent third party or the manager, operator or control entity must be appointed to carry out title verification as described above.

A private fund must appoint either an administrator, custodian or another independent party or the manager, operator or control entity to monitor cash flows, ensure that all cash has been booked in the cash accounts and ensure that all payments made by investors have been received.

____________________________

- “Non-fund arrangements” include, for example, joint ventures, proprietary vehicles, debt issues and debt issuing vehicles, structured finance vehicles, occupational and personal pension schemes, sovereign wealth funds, single family offices and funds whose investment interests are listed on stock exchanges specified by CIMA.

- The first-year annual registration fee of approximately US$4,270 will not be payable for Cayman entities which have registered as “private fund” by August 7, 2020.

![]()

E: Piers.Alexander@conyers.com

T: (852) 2842 9525

Conyers

Conyers Christopher Bickley

Christopher Bickley