By Michael Taylor of Coldwater Economics

E: mtaylor@coldwatereconomics.com

Hong Kong, its relatively short history replete with chapters of lucrative self-discovery, is at the advent of its greatest transformation yet, a convergence with neighbouring Shenzhen that is set to be one of the two or three most vital growth stories of the next decade.

Perhaps even more surprising, this Hong Kong/Shenzhen powerhouse has every prospect of becoming the pre-eminent centre of the world’s data economy, possibly eclipsing at some point in the none-too-distance future even the San Francisco Bay Area.

Curiously, though, the dynamics of this latest re-invention and the potential scale of the economic spoils are as yet largely unacknowledged in the territory itself or by the financial industry that occupies its gleaming towers. Needless to say, if the rest of the world spares any attention at all for Hong Kong it is likley to focus only on political and generational discontents (which, while real and unignorable in the local context, are irrelevant to the economic crucible across the border).

Hong Kong is never what it used to be: every twist and turn of China’s history has added to the mix. In the 1940s and 1950s, Hong Kong received industrialists, financiers and chancers from all over China declining the Communist Revolution. In the 1960s, a greater influx of refugees fleeing the chaos of the Cultural Revolution arrived in town, with the British authorities instituting an immigration policy not a million miles away from a game of tag (if you could get to Kowloon police station without being nabbed, you were in). Thus was Hong Kong established as a cheap manufacturing centre. When China began to open up under Deng Xiaoping, Hong Kong’s purpose shifted too, becoming for a time the world’s busiest port facilitating and financing trade with China. In the 1990s the port business was slowly eclipsed by Hong Kong’s growing role as Asia’s premier ex-Japan international financial centre.

The change which is now underway will put Hong Kong at the centre of the emerging global data-economy. And it will do that through convergence with its neighbour Shenzhen.

Ever since Shenzhen’s economy was dreamed into life in the 1980s by Chinese businessmen and technocrats arriving from across China, having been given their head by Deng Xiaoping, Hong Kong has looked upon it with a mixture of scorn and temptation. It couldn’t, obviously, compete with Hong Kong, but as a cheap and convenient place to locate your business, or your mistress, it had a lot going for it.

But Shenzhen has rapidly grown into something far different, and far bigger, than that. No longer merely a cheap manufacturing centre, its commercial and technological footprint now includes global players such as Tencent, ZTE, Huawei, BYD, and gene-sequencer BIG, as well as a myriad and proliferating bunch of tech and research-related start-ups. And, quite suddenly, the logic of full-blooded commercial and financial convergence between these two neighbouring economies has become irresistible. The fact that there are plenty of people in Hong Kong who are nervous of the prospect it itself telling: the city which prides itself as the most capitalist in the world is looking over its shoulder at a serious contender.

One way to monitor the convergence is simply to acknowledge how Shenzhen’s has grown to rival Hong Kong’s, and is poised to overtake it. In 2007, at prevailing exchange rates, Hong Kong’s economy was about 2.4x the size of Shenzhen’s; by 2017, they were roughly the same size. That convergence is not because Hong Kong has slowed down, but because Shenzhen has just kept growing so quickly.

And Shenzhen’s GDP growth is not merely the result of adding rapidly to its population: Hong Kong has a population of 7.3mn with a per capital GDP of approximately $46,000; Shenzhen now has a population of just under 12m with a per capita GDP of around $27,000.

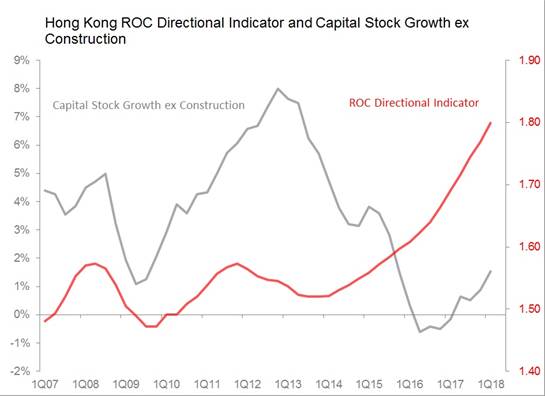

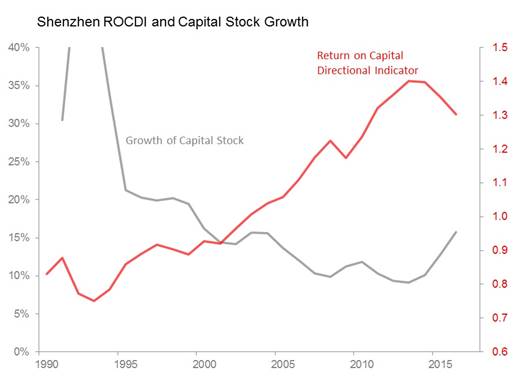

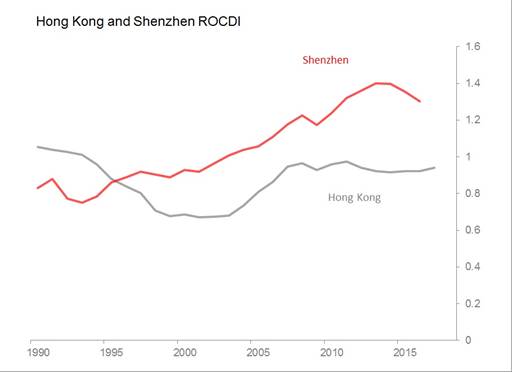

But we can illustrate the economic logic that’s driving convergence more directly, by comparing trends in return on capital in both Hong Kong and Shenzhen. Whilst one cannot do this directly, one can generate a return on capital directional indicator (ROCDI) by expressing nominal GDP as a flow of income from a stock of fixed capital, and by estimating changes in that stock of capital by depreciating all gross fixed investment over a 10 year period.

The story for Hong Kong between 2012 and the present day has been one in which Hong Kong has, until very recently, been reluctant to invest, but has preferred rather to sweat its existing assets ever harder in order to raise return on capital to historic highs. Over in Shenzhen, meanwhile, the growth of capital stock has been maintained, but never until the last couple of years has the accumulation of capital stock threatened to dampen the return on that capital. I should add that Shenzhen’s model of growth in this respect has been almost the exact opposite of China’s strategy, which until very recently has prioritized growth of capital stock above virtually everything else (and certainly above return on capital).

What has emerged over the last couple of years is that the trends in ROCDI are finally beginning to converge between Hong Kong and Shenzhen. The arbitrage possibilities between returns on capital in Hong Kong and Shenzhen really are enough to explain the different patterns which are emerging. Although Hong Kong’s return on capital is at a historically high point, it is below that of Shenzhen. It therefore makes more sense for Hong Kong to invest in Shenzhen. And so, whilst this has delayed the re-investment in Hong Kong until the last year, it has reignited investment spending in Shenzhen into 20%+ levels, even at a time when overall investment spending in China has been slowing sharply.

As time goes on, we can expect this investment arbitrage to continue to raise the rate of Hong Kong’s ROCDI from existing levels, whilst reducing Shenzhen’s. As that convergence becomes more effective, the disparity between rates of investment in Shenzhen and Hong Kong will also converge.

In other words, for Hong Kong the immediate prospect is for return on capital to keep rising, and the growth of that capital stock itself to accelerate. This is the very stuff of positive business cycles, and profits generation.

But that is merely the beginning of the opportunity, because taken together as a single economy, Hong Kong / Shenzhen is already surprisingly significant in global terms. In 2018, at current exchange rates, the Hong Kong / Shenzhen will have a combined GDP of around US$724bn. In global terms, that’s bigger than Switzerland, bigger than Saudi Arabia, and about the size of the Netherlands. In terms of the US, it’s about the same size as Pennsylvania, which is the sixth largest state in the US. It is also, already, knocking on the door of the entire US Bay Area economy. It will overtake it soon enough: during the last 10 years, which includes the financial crisis, it has averaged nominal GDP growth of 8.5% a year.

What are the preconditions that are allowing this convergence to take place? The usual: movement of capital, movement of people, and movement of ideas sufficient to let profitable arbitrage take place. All these are already broadly in place, and government policies on both sides of the border are supporting greater integration. The stock and bond connect programs which link Hong Kong and Shenzhen equity markets are turning over approximately HK$7bn a day, with buying into Shenzhen being the dominant feature. Hong Kong’s banking system essentially takes in deposits from mainland companies and citizens, and re-lends those back into the mainland banking system.

As for movement of people, the border is busy: the border crossing between Hong Kong and Shenzhen handles 44k vehicle crossings a day, with Lo Wu handling processing 250k people each day. And that’s just vehicles: the MTR runs trains to Lo Wu every six to eight minutes, the journey takes just under and hour and costs about US$5.

Finally, there is the movement of ideas. At this point, the pool Shenzhen is fishing in is truly global. First, from the beginning Shenzhen has attracted talent from all over China, not just Hong Kong or Guangdong. Now it is also not only attracting talent from around the world, it is growing its own educational and R&B infrastructure extremely rapidly. It is also ploughing money into research and development to accelerate the process: Hong Kong spends 0.73% of GDP on R&D, China spends 2.07%, but Shenzhen spends 4.7%. As for education spending, to take one example, Shenzhen is home to the Peking University School of Transnational Law which offers its students grounding not just in Chinese law, but also in American law via a Juris Doctor (JD) program.

What is Hong Kong’s specific role to be in this convergence? Plenty of people in Hong Kong cannot quite imagine how it will compete. But two things seem likely. First, at the core of the Hong Kong /Shenzhen convergence will be the discovery of what a ‘data-economy’ can be, and can achieve. If data is the core feedstock of the new economy, China is the biggest source of the lot, and plenty of companies will want to go mining there. However, worries about the legitimate use of data will predictably morph into the desire to protect national data, if only for national security reasons. In such a world, Hong Kong’s history of trading and finance bequeaths it a history of international legitimacy that Shenzhen and its partners could use.

That seems a logical trajectory, but of course, Hong Kong may discover quite different advantages during the convergence. And, crucially, just as the numbers tells us that convergence is already underway, so the numbers also tells us that Hong Kong is discovering new sources of advantage. We can see this in Hong Kong’s renewed ability to price its services export internationally. Between early 2012 and late 2016 Hong Kong became unable to raise the price of its services exports: a crucial failure given Hong Kong’s raison d’etre as an international services centre. But from late 2016, as investment patterns revealed the acceleration of convergence with Shenzhen, this changed, with services export prices rising 9.5% since 3Q16. The process of discovering its new role in the Hong Kong / Shenzhen economy will throw up so-far unthought-of profit opportunities.

A final thought: the Hong Kong / Shenzhen convergence is a story not yet told. In Hong Kong itself, the incumbent private sector rulers of its existing economy don’t particularly want to talk about it; the foreign business community in any case rarely strays outside Central’s towers; the government itself doesn’t have much to say about it. And yet, the numbers don’t lie, and, more, when you confront Hong Kongers with them, the light goes on, and there is that unfakeable moment of recognition of an obvious truth. History is running in Hong Kong again.